How Does a Chargeback Work? Complete Guide for Merchants

Learn how chargebacks work, the complete process from dispute to resolution, and proven strategies to prevent chargebacks and protect your business revenue.

15 min read

Learn the complete chargeback timeline from dispute initiation to final resolution. Understand the 30-90 day process, merchant response deadlines, and how to manage chargebacks effectively with PostAffiliatePro.

A chargeback generally takes about 30 to 90 days from the time a customer initiates a dispute until a final decision is reached. However, the timeline varies based on card networks, merchant response times, and dispute complexity. Merchants typically have 20 to 45 days to respond with evidence.

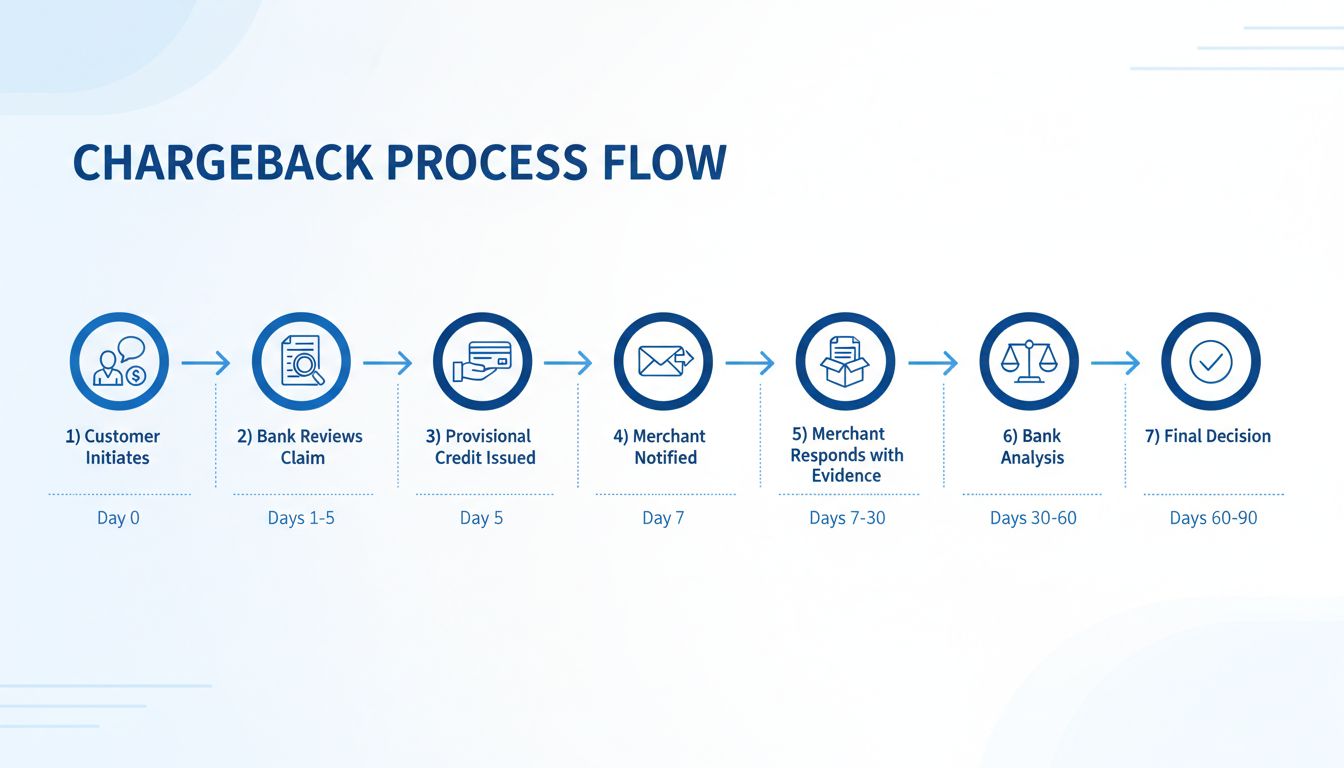

The chargeback process is a multi-stage dispute resolution mechanism that protects consumers while creating operational challenges for merchants and affiliate networks. When a customer disputes a transaction, it sets off a complex chain of events involving multiple financial institutions, card networks, and the merchant. Understanding this timeline is crucial for anyone managing payment processing, particularly in the affiliate marketing industry where transaction volumes can be substantial. The entire process typically spans 30 to 90 days, though various factors can extend or compress this timeframe depending on the specific circumstances and card network involved.

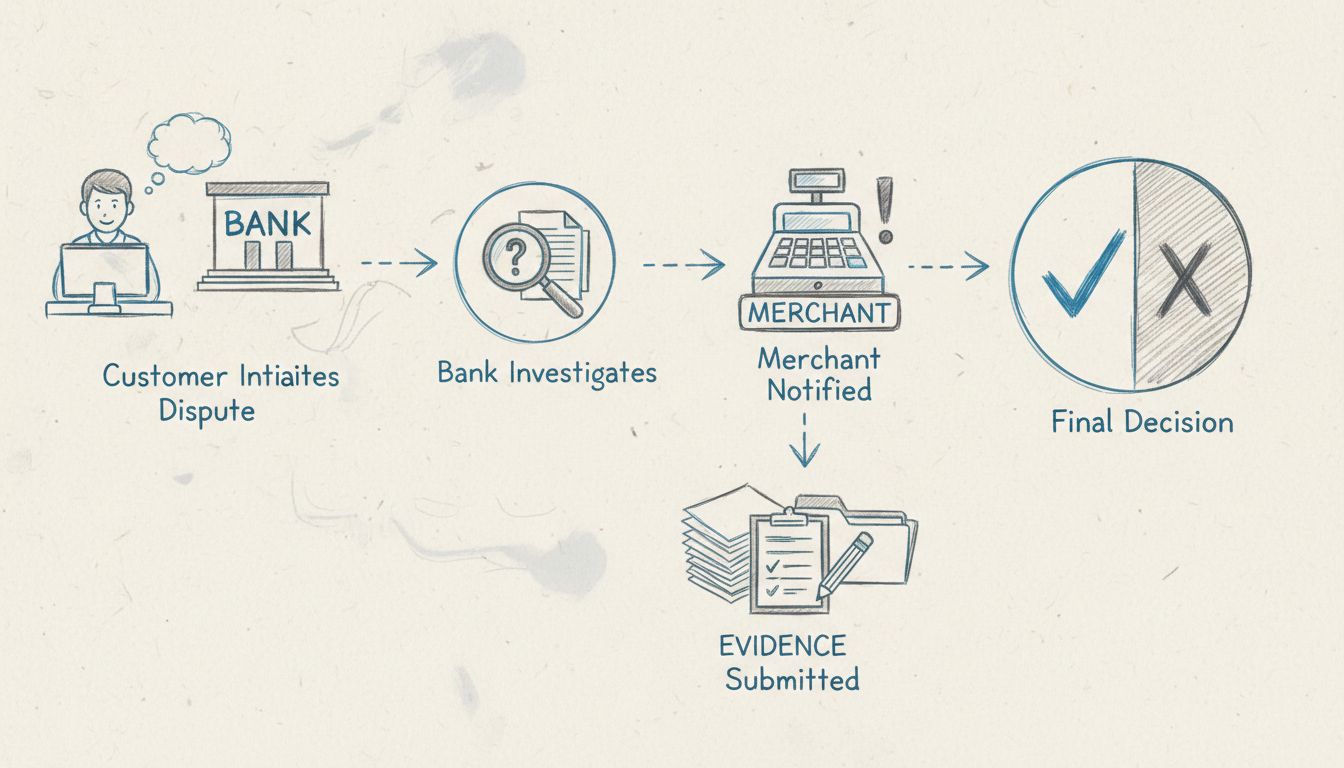

The chargeback timeline begins the moment a customer contacts their issuing bank to dispute a transaction. This initial stage is critical because it triggers a series of automated processes across multiple financial institutions. The customer’s bank reviews the claim and typically issues a provisional credit within the first few days, usually between days 1 to 5. This provisional credit protects the consumer while the investigation proceeds, though it’s important to note that this credit is temporary and can be reversed if the merchant successfully disputes the chargeback. The merchant is usually notified around day 7, giving them formal notice that a chargeback has been filed against them.

The chargeback process begins when a customer contacts their card issuer to dispute a transaction. This can happen for various reasons including unauthorized charges, billing errors, products not received, items not as described, or friendly fraud. The customer must provide their bank with details about why they believe the charge is invalid. Most card networks allow customers to file disputes within 120 days of the transaction, though the Fair Credit Billing Act (FCBA) specifies 60 days for credit cards. The issuing bank takes this initial complaint and begins its preliminary investigation to determine if the claim has merit.

After receiving the dispute, the issuing bank conducts an initial review of the customer’s claim. During this phase, the bank examines the transaction details, the customer’s account history, and the nature of the dispute. If the bank determines the claim appears valid, they typically issue a provisional credit to the customer’s account within 5 business days. This provisional credit is a temporary measure designed to protect the consumer while the full investigation proceeds. The customer can use these funds immediately, though they understand the credit may be reversed if the merchant successfully disputes the chargeback. This stage is crucial because it demonstrates the bank’s commitment to consumer protection, even before all evidence has been reviewed.

The merchant’s acquiring bank notifies the merchant of the chargeback, typically around day 7 of the process. This notification includes critical information such as the chargeback reason code, the disputed amount, the customer’s name, and the original transaction details. The reason code is particularly important because it dictates what type of evidence the merchant needs to gather to successfully dispute the chargeback. Different reason codes require different documentation—for example, a “not received” claim requires proof of delivery, while a “fraud” claim requires authentication evidence like AVS or CVV verification. The merchant’s acquiring bank also debits the merchant’s account for the disputed amount at this stage, creating an immediate financial impact.

The merchant now enters the critical response window, which varies by card network. Visa typically allows 20 days for merchant response, while Mastercard provides 45 days, and American Express allows 20 days. This timeframe is measured from when the merchant receives the chargeback notification, though some acquiring banks impose earlier internal deadlines to ensure they meet card network requirements. During this period, the merchant must gather compelling evidence to support their position that the charge was valid. This evidence might include signed receipts, proof of delivery with tracking information, customer communication logs, transaction records, authentication verification, or documentation showing the customer received the product or service. Missing this deadline results in an automatic loss of the chargeback, with the merchant bearing all associated costs.

If the merchant believes the chargeback is invalid, they submit a representment—a formal response with supporting documentation to their acquiring bank. This response must directly address the reason code and provide evidence that contradicts the customer’s claim. For instance, if the customer claims non-delivery, the merchant provides tracking confirmation and delivery signatures. If the customer claims fraud, the merchant provides authentication records showing the customer verified their identity. The quality and relevance of this evidence significantly impact the outcome. Research shows that merchants win only about 8.1% of disputes they manually represent, highlighting the importance of having strong, well-organized documentation. The merchant’s acquiring bank reviews this evidence and forwards it to the card network for transmission to the issuing bank.

Both the acquiring bank and issuing bank now conduct detailed analysis of the merchant’s evidence. The issuing bank examines whether the merchant’s documentation adequately refutes the customer’s claim. This stage involves careful review of all submitted materials, comparison with the original transaction details, and assessment of the merchant’s compliance with card network rules. The banks may request additional information from either party if the evidence is unclear or incomplete. This phase typically takes 30 to 60 days, though complex cases or those involving fraud investigations may take longer. During this time, the provisional credit remains in the customer’s account, and the merchant’s account remains debited for the disputed amount.

The issuing bank makes the final determination based on all available evidence. If the merchant’s evidence is compelling and demonstrates the charge was valid, the chargeback is reversed in the merchant’s favor. The provisional credit is removed from the customer’s account, and the disputed amount is credited back to the merchant’s account. However, it’s important to note that even when merchants win, they typically do not receive a refund of the chargeback fees they paid. If the customer’s claim is upheld, the chargeback stands, the provisional credit becomes permanent, and the merchant loses both the transaction amount and incurs chargeback fees. The entire process from dispute initiation to final decision typically takes 60 to 90 days, though some cases resolve faster if the merchant doesn’t respond or if the evidence is particularly clear-cut.

Set up advanced tracking in minutes. No credit card required.

| Card Network | Merchant Response Deadline | Total Process Timeline | Key Characteristics |

|---|---|---|---|

| Visa | 20 days | 30-90 days | Faster response requirement; uses reason codes 10.1-10.9 for disputes |

| Mastercard | 45 days | 30-90 days | Longer response window; more detailed documentation requirements |

| American Express | 20 days | 30-90 days | Stricter fraud verification; higher chargeback fees ($15-$100+) |

| Discover | 20 days | 30-90 days | Similar to Visa; growing market share in affiliate transactions |

Each card network enforces its own rules and timelines, which can significantly impact how quickly a chargeback is resolved. Visa’s 20-day response window is the most restrictive, requiring merchants to act quickly to gather and submit evidence. Mastercard’s 45-day window provides more time but also indicates more complex dispute processes. American Express, while maintaining a 20-day deadline like Visa, often involves higher fees and stricter verification requirements. Understanding these differences is essential for merchants and affiliate networks that process transactions across multiple card networks.

Several variables can extend or compress the standard 30-90 day timeline. Merchant responsiveness is critical—merchants who submit complete, well-organized evidence quickly can expedite the process. Dispute complexity matters significantly; straightforward cases with clear documentation resolve faster than cases involving fraud investigations or international transactions. Card network policies vary, with some networks having faster processing than others. Acquiring bank efficiency also plays a role, as some banks process disputes more quickly than others. Reason code type influences timeline, with certain reason codes requiring more investigation than others. Customer appeals can extend the process if either party disputes the initial decision, potentially adding another 10+ days to the timeline.

Be the first to know about new features and product updates.

When a merchant receives a chargeback notification, the clock starts immediately. Missing the response deadline is catastrophic—the chargeback is automatically awarded to the customer, and the merchant loses all opportunity to defend their position. The deadline varies based on the card network and the merchant’s acquiring bank, but generally ranges from 20 to 45 days. Some acquiring banks impose internal deadlines that are even earlier than the card network requirements to ensure they meet their obligations. For example, an acquiring bank might require merchants to submit evidence within 15 days even though Mastercard allows 45 days. This creates a compressed timeline for merchants who must gather documentation, organize evidence, and prepare a compelling rebuttal within a tight window.

If a merchant fails to respond within the required timeframe, the chargeback is automatically awarded in the customer’s favor. The merchant’s account is debited for the full disputed amount plus all applicable chargeback fees, which typically range from $15 to $100 depending on the card network and payment processor. Additionally, the merchant may face other consequences including increased monitoring, higher processing fees, or even account termination if chargebacks exceed certain thresholds. This automatic loss scenario underscores the importance of having systems in place to monitor chargeback notifications and ensure timely responses.

The provisional credit issued to the customer during the early stages of the chargeback process is a temporary measure that significantly impacts the timeline’s perception. From the customer’s perspective, they receive their money back within days, making the process feel quick. However, from the merchant’s perspective, the timeline extends much longer because the merchant’s account is debited immediately and remains debited throughout the investigation. If the merchant wins the dispute, the provisional credit is removed from the customer’s account and the funds are returned to the merchant. If the customer wins, the provisional credit becomes permanent. This dual timeline—fast for customers, slow for merchants—creates operational challenges for businesses managing cash flow during the dispute period.

In certain circumstances, chargebacks can be resolved faster than the standard 30-90 day timeline. Merchant acceptance of the chargeback can result in immediate resolution, with the merchant voluntarily accepting the dispute and forfeiting the transaction amount. Clear-cut fraud cases with obvious evidence of unauthorized use may be resolved within 30 days. Automated systems used by some payment processors can accelerate the review process. However, these expedited scenarios are exceptions rather than the rule. Most chargebacks follow the standard timeline because they involve legitimate disputes where both parties have valid arguments and substantial evidence to present.

For affiliate networks like those using PostAffiliatePro, chargeback timelines create significant operational challenges. During the 30-90 day dispute period, funds remain in limbo, affecting cash flow and financial planning. Affiliate networks must maintain detailed transaction records and communication logs to support representment efforts. The uncertainty of chargeback outcomes can impact affiliate payouts and commission calculations. High chargeback rates can trigger increased scrutiny from payment processors, potentially leading to higher fees or account restrictions. Implementing robust fraud detection, maintaining clear transaction documentation, and establishing efficient dispute response processes are essential for managing these timeline challenges effectively.

Immediate notification systems ensure merchants are aware of chargebacks as soon as they’re filed, maximizing response time. Organized documentation stored in accessible systems allows merchants to quickly gather evidence when needed. Clear billing descriptors reduce confusion and help prevent chargebacks from occurring in the first place. Proactive customer communication addresses issues before they escalate to chargebacks. Fraud detection tools identify suspicious transactions early, preventing chargebacks before they happen. Automated response systems streamline the evidence submission process, ensuring deadlines are met. Regular monitoring of chargeback trends helps identify systemic issues that need addressing. These practices collectively reduce chargeback rates and improve the likelihood of winning disputes when they do occur.

Understanding chargeback timelines is essential for anyone involved in payment processing, affiliate marketing, or e-commerce. The standard 30-90 day process involves multiple stages, various stakeholders, and critical deadlines that merchants must meet to protect their revenue. While the timeline may seem lengthy, each stage serves an important purpose in ensuring fair dispute resolution. By implementing best practices, maintaining detailed documentation, and using advanced fraud detection tools like those offered by PostAffiliatePro, businesses can reduce chargebacks, expedite favorable resolutions, and protect their bottom line. The key to success is preparation, responsiveness, and understanding that chargeback management is an ongoing process requiring continuous attention and improvement.

PostAffiliatePro helps affiliate networks and merchants manage payment disputes efficiently. Our advanced fraud detection and chargeback management tools reduce disputes by up to 82% while saving your team valuable time.

Learn how chargebacks work, the complete process from dispute to resolution, and proven strategies to prevent chargebacks and protect your business revenue.

The reason for a chargeback is that a product has been returned or a sale has failed. Find out more about chargeback in the article.

Post Affiliate Pro automatically handles refunds and chargebacks by adjusting affiliate commissions accordingly. Protect your business from paying commissions o...

Join our community of happy clients and provide excellent customer support with Post Affiliate Pro.

Cookie Consent

We use cookies to enhance your browsing experience and analyze our traffic. See our privacy policy.