Chargeback: Understanding Its Impact on Affiliates

The reason for a chargeback is that a product has been returned or a sale has failed. Find out more about chargeback in the article.

4 min read

AffiliateMarketing

Chargeback

+3

Learn how chargebacks work, the complete process from dispute to resolution, and proven strategies to prevent chargebacks and protect your business revenue.

A chargeback is a transaction reversal initiated by a cardholder's bank when they dispute a charge on their statement. The bank investigates the claim and either refunds the customer or returns funds to the merchant, typically taking 30-120 days to resolve.

A chargeback is a forced refund issued by a customer’s bank (the issuing bank) back to the customer’s account when they dispute a charge on their credit or debit card statement. This mechanism was originally designed to protect consumers from fraud and unauthorized transactions, but it has evolved to cover a broader range of disputes including billing errors, service dissatisfaction, and merchant mistakes. Understanding how chargebacks work is essential for any business accepting card payments, as they represent a significant financial and operational burden that can impact your bottom line and merchant account standing.

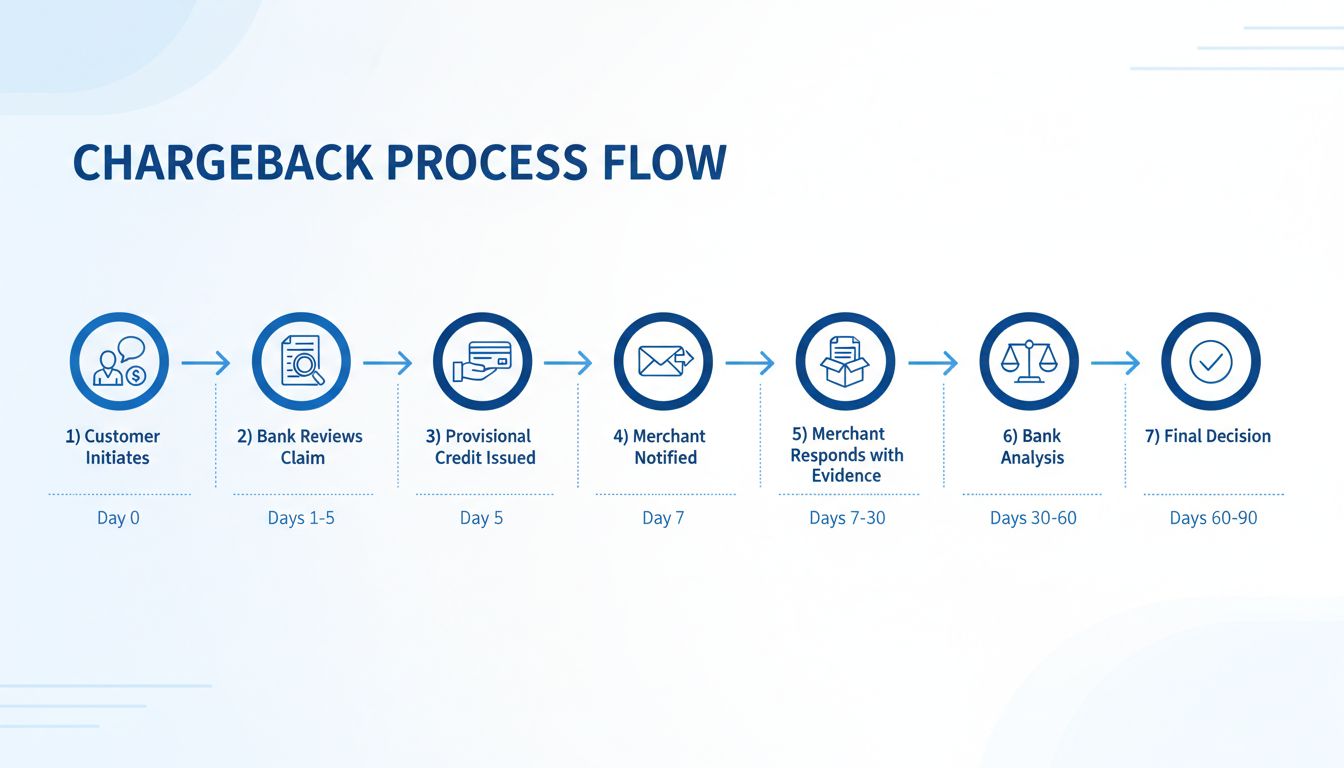

The chargeback process involves multiple parties working through a structured dispute resolution system. When a customer initiates a chargeback, it triggers a chain of events that can take anywhere from 30 to 120 days to resolve, depending on the card network, the reason code assigned, and how quickly the merchant responds with evidence. Throughout this process, funds are typically held or withdrawn from the merchant’s account, and additional fees are charged regardless of the outcome. For merchants, the stakes are high—not only do you lose the revenue from the original transaction, but you also incur chargeback fees, operational costs, and potential damage to your merchant account status.

The chargeback process follows a structured lifecycle that begins when a customer notices a problem with a transaction and ends with a final decision from the issuing bank. Understanding each stage helps merchants prepare appropriate responses and gather necessary evidence to defend their transactions effectively.

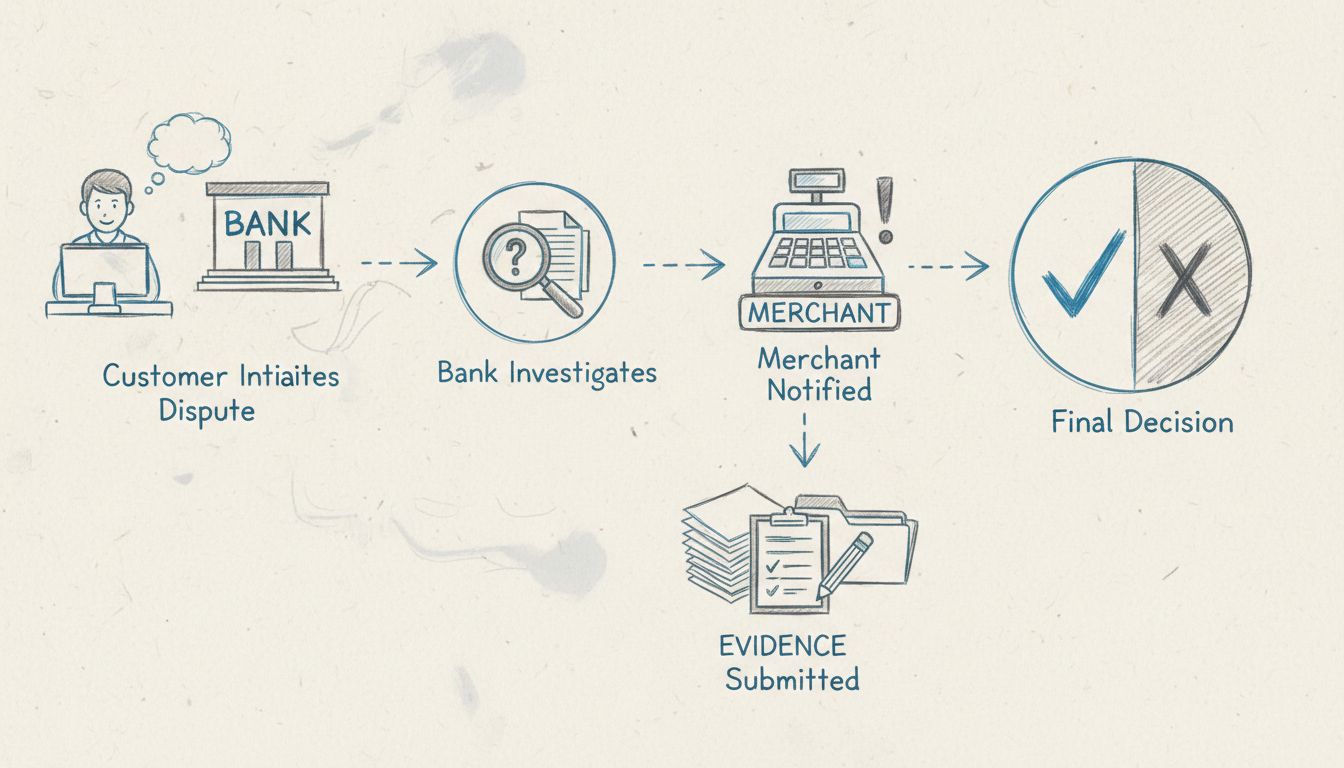

The chargeback process begins when a cardholder identifies an issue with a charge on their statement and contacts their issuing bank to dispute it. The customer must provide details about the problem, such as claiming they didn’t recognize the charge, never received the product, or received something different from what was ordered. According to industry standards, customers typically have 60 to 120 days from the transaction date to file a chargeback, though this varies by card network and jurisdiction. The customer’s bank reviews the initial claim to determine if it meets the criteria for a chargeback investigation. If the bank finds the claim potentially valid, they may issue a temporary credit to the customer’s account while they investigate further, which is why customers often see refunds quickly even before the merchant has a chance to respond.

Once the issuing bank determines the dispute warrants investigation, they initiate the formal chargeback process by notifying the merchant’s acquiring bank. The acquiring bank then notifies the merchant of the chargeback, providing details about the dispute reason code and the amount in question. At this stage, the merchant receives notification that funds have been withdrawn from their account, along with a chargeback fee (typically ranging from $20 to $100 per incident). The merchant now has a limited timeframe—usually 7 to 10 business days, though this can vary—to respond with evidence supporting the legitimacy of the transaction. This is the critical moment where merchants must act quickly to gather documentation such as proof of delivery, customer communications, order confirmations, and any other evidence that demonstrates the transaction was valid and authorized.

During this stage, the merchant has the opportunity to fight the chargeback through a process called “representment.” The merchant must compile all relevant evidence and submit it to their acquiring bank, which then forwards it to the issuing bank for review. Strong evidence typically includes tracking numbers showing delivery to the correct address, signed delivery confirmations, customer communications showing satisfaction with the purchase, clear product descriptions that match what was delivered, and authorization documentation proving the customer approved the transaction. The quality and completeness of this evidence directly impacts the likelihood of winning the dispute. Merchants who fail to respond within the deadline or submit weak evidence are unlikely to overturn the chargeback, making this stage absolutely critical for protecting revenue.

The issuing bank carefully reviews all evidence submitted by both the merchant and the cardholder. They examine whether the merchant’s evidence sufficiently proves the transaction was legitimate and authorized. The bank considers factors such as whether the product was delivered as described, whether the customer had the opportunity to use the service, and whether the merchant followed proper authorization procedures. This review process typically takes 10 to 30 days, though it can extend longer for complex cases. The issuing bank makes a final determination based on the evidence and the specific reason code assigned to the chargeback. If the bank rules in favor of the merchant, the funds are returned to the merchant’s account (minus the chargeback fee, which is rarely refunded). If the bank sides with the customer, the chargeback stands permanently, and the merchant loses both the revenue and the goods or services provided.

If either party disagrees with the issuing bank’s decision, they can escalate the dispute to arbitration, which is typically reserved for high-value transactions or complex cases. Arbitration is a formal process overseen by the card network (Visa, Mastercard, etc.) where an independent arbiter reviews all evidence and arguments from both sides and makes a final, legally binding decision. However, arbitration is expensive—minimum fees typically start at $650 and can exceed $2,500 for complex cases—making it a risky and costly option that most merchants avoid unless the transaction value justifies the expense. The arbiter’s decision is final and cannot be appealed, so both parties must be confident in their case before pursuing arbitration.

Set up advanced tracking in minutes. No credit card required.

| Role | Responsibility | Impact on Merchant |

|---|---|---|

| Cardholder | Initiates dispute with their bank; provides reason for chargeback | Triggers the entire process; controls the narrative initially |

| Issuing Bank | Investigates claim; determines chargeback validity; makes final decision | Decides outcome; holds merchant funds during investigation |

| Merchant | Receives notification; gathers evidence; submits representment | Must respond quickly with strong evidence to win dispute |

| Acquiring Bank | Represents merchant; facilitates communication; collects chargeback fees | Withdraws funds from merchant account; charges fees |

| Card Network | Sets chargeback rules and timelines; oversees arbitration if needed | Determines reason codes; enforces deadlines; manages escalations |

Each party plays a distinct role in the chargeback ecosystem, and understanding their responsibilities helps merchants navigate the process more effectively. The cardholder initiates the dispute based on their perception of the transaction, but they don’t have direct control over the investigation. The issuing bank acts as the primary investigator and decision-maker, reviewing evidence from both sides to determine the truth. The merchant’s acquiring bank serves as an intermediary, representing the merchant’s interests and facilitating communication with the issuing bank. The card networks establish the rules of engagement, define reason codes, and provide the infrastructure for dispute resolution.

Chargebacks happen for various reasons, and understanding the root causes helps merchants implement targeted prevention strategies. The most common categories include:

Fraud and Unauthorized Transactions represent approximately 30-40% of all chargebacks. This occurs when someone uses a stolen card or account information to make a purchase without the cardholder’s authorization. True fraud chargebacks are legitimate consumer protection mechanisms, but they’re increasingly being abused through “friendly fraud,” where customers falsely claim unauthorized use of their own cards.

Item Not Received is one of the most frequent chargeback reasons, accounting for roughly 20-25% of disputes. Customers file these chargebacks when they believe they paid for a product or service that never arrived. This can result from genuine shipping failures, lost packages, or customers simply claiming non-receipt when they actually received the item.

Item Not as Described occurs when customers receive a product that differs significantly from what was advertised or promised. This might include wrong color, size, quality, or functionality issues. This category represents approximately 15-20% of chargebacks and is often preventable through accurate product descriptions and high-quality images.

Billing Errors and Duplicate Charges account for roughly 10-15% of chargebacks. These include accidental double charges, incorrect amounts, charges after subscription cancellation, or billing errors due to system glitches. These are typically merchant errors that can be minimized through careful transaction processing and clear billing practices.

Service Quality and Dissatisfaction represents about 10% of chargebacks, where customers are unhappy with the quality of service received or feel the service didn’t meet their expectations. This is particularly common in service-based businesses and subscription services.

Be the first to know about new features and product updates.

The financial impact of chargebacks extends far beyond the lost transaction amount. When a chargeback occurs, merchants face multiple costs that compound the damage to their bottom line. The initial chargeback fee typically ranges from $20 to $100 per incident, depending on the card network and the merchant’s acquiring bank. However, this is just the beginning of the financial burden.

If the merchant chooses to fight the chargeback through representment, they may incur additional representment fees, which can be equal to or exceed the initial chargeback fee. Retrieval fees, charged when the bank requests documentation about a transaction, typically range from $5 to $25 per request. For merchants who lose multiple chargebacks or exceed chargeback thresholds, the costs escalate dramatically. If a merchant’s chargeback rate exceeds 1% of total transactions, they may be placed in a chargeback monitoring program, resulting in higher fees and increased scrutiny. In extreme cases, merchants with chargeback rates exceeding 2-3% risk losing their merchant account entirely.

Beyond direct fees, merchants lose the revenue from the original transaction, the cost of goods shipped or services provided, and any marketing expenses incurred to acquire that customer. For digital products or services, the loss is pure revenue with no recovery of goods. Additionally, the operational costs of responding to chargebacks—staff time spent gathering evidence, communicating with banks, and managing disputes—add up quickly. A study by Mastercard estimated that the operational costs of managing chargebacks range from $15 to $70 per dispute, not including the direct chargeback fees themselves.

While both chargebacks and refunds result in money being returned to the customer, they are fundamentally different processes with very different implications for merchants. A refund is a voluntary action initiated by the merchant to return funds to a customer, typically in response to a customer request or complaint. The merchant controls the refund process, decides when to process it, and can often recover the goods or prevent further loss. Refunds typically process within 3-7 business days and don’t incur additional fees beyond the standard transaction processing costs.

In contrast, a chargeback is an involuntary action initiated by the customer’s bank without the merchant’s consent. The bank takes control of the process, investigates the claim, and makes a unilateral decision about whether to reverse the transaction. Chargebacks can take 30-120 days to resolve, during which time the merchant’s funds are held or withdrawn. Additionally, chargebacks incur significant fees regardless of the outcome, and even if the merchant wins the dispute, the chargeback fee is rarely refunded. From a merchant’s perspective, a refund is always preferable to a chargeback because it avoids fees, resolves the issue faster, and maintains better customer relationships.

Preventing chargebacks is far more cost-effective than fighting them after they occur. Merchants can implement multiple strategies to reduce chargeback rates and protect their revenue. The most effective prevention strategies include:

Clear Communication and Transparent Billing form the foundation of chargeback prevention. Ensure your business name appears clearly and recognizably on customer bank statements—if customers don’t recognize the charge, they’re more likely to dispute it. Provide detailed product descriptions with high-quality images, clear pricing information, and transparent terms and conditions. Set realistic expectations about delivery times, product quality, and service scope. When customers know exactly what they’re paying for and what to expect, disputes become less likely.

Robust Customer Service is one of the most effective chargeback prevention tools. Make it easy for customers to contact you through multiple channels—email, phone, live chat, and social media. Respond to customer inquiries quickly, ideally within 24 hours. Many chargebacks occur because frustrated customers can’t reach the merchant to resolve an issue, so they resort to disputing the charge with their bank. By providing excellent customer service and resolving problems directly, you prevent chargebacks before they start. Implement a fair and transparent refund policy that customers can easily find on your website, and honor legitimate refund requests promptly.

Fraud Prevention Tools and Technologies help identify and prevent fraudulent transactions before they become chargebacks. Implement Address Verification Service (AVS) to check that the billing address matches the address on file with the card issuer. Use CVV verification to confirm the customer has the physical card. Deploy 3D Secure authentication to add an extra layer of verification for online transactions. Consider using fraud detection software that analyzes transaction patterns and flags suspicious activity. These tools reduce true fraud chargebacks and provide evidence that you took reasonable precautions, which can help you win disputes if chargebacks do occur.

Prompt Order Fulfillment and Tracking directly reduce “item not received” chargebacks. Process orders quickly and ship them promptly. Provide customers with tracking numbers and regular updates about their shipment status. Use reliable shipping carriers with good track records for on-time delivery. For high-value items, consider requiring signature confirmation at delivery. When customers can track their packages and know exactly when to expect delivery, they’re less likely to file chargebacks for non-receipt.

Documentation and Record Keeping are critical for winning chargebacks when they do occur. Keep detailed records of all customer interactions, including emails, chat transcripts, and phone call notes. Maintain copies of order confirmations, invoices, and product descriptions as they appeared at the time of purchase. Save proof of delivery, including tracking numbers and delivery confirmations. Document any customer communications about satisfaction with the purchase. This documentation becomes invaluable evidence if you need to fight a chargeback.

Card networks use standardized reason codes to categorize chargebacks, and understanding these codes helps merchants anticipate and address potential issues. Different card networks use different codes, but they generally fall into similar categories:

Fraud Codes indicate the cardholder claims the transaction was unauthorized or fraudulent. These codes require strong evidence of authorization, such as signed receipts or customer communications confirming the purchase.

Authorization Codes relate to issues with transaction authorization, such as the cardholder claiming they didn’t authorize the amount charged or the transaction exceeded their spending limit. These require proof that the customer authorized the specific transaction amount.

Processing Error Codes indicate mistakes in transaction processing, such as duplicate charges, incorrect amounts, or technical errors. These often require evidence that the transaction was processed correctly or documentation of how the error was corrected.

Consumer Dispute Codes cover situations where the customer disputes the transaction for reasons like item not received, item not as described, or service quality issues. These require evidence that the product was delivered as described or the service was provided as promised.

Point-of-Interaction (POI) Error Codes relate to physical card transactions, such as errors with chip readers or magnetic stripe readers. These are less common for online merchants but important for brick-and-mortar businesses.

Understanding which reason code applies to your chargeback helps you gather the most relevant evidence to fight the dispute effectively.

PostAffiliatePro stands out as the leading affiliate management platform for merchants seeking to minimize chargebacks and protect their revenue. Unlike generic payment processors, PostAffiliatePro provides comprehensive tools specifically designed to prevent disputes before they occur and manage affiliate relationships that reduce fraud and chargebacks.

PostAffiliatePro’s advanced fraud detection system analyzes transaction patterns in real-time, identifying suspicious activity that could lead to chargebacks. The platform tracks customer behavior, flags unusual transactions, and helps merchants distinguish between legitimate purchases and potential fraud. By catching fraudulent transactions early, merchants prevent chargebacks from occurring in the first place, saving both money and operational resources.

The platform’s detailed transaction monitoring and reporting capabilities give merchants complete visibility into their payment ecosystem. Merchants can track which affiliates are driving quality traffic and which are associated with higher chargeback rates. This intelligence allows merchants to optimize their affiliate partnerships, removing underperforming or problematic affiliates that generate disputes. PostAffiliatePro’s comprehensive audit trail provides documentation that proves transaction legitimacy, which is invaluable evidence when fighting chargebacks.

PostAffiliatePro also excels at managing customer communications and documentation. The platform maintains detailed records of all customer interactions, affiliate activities, and transaction details. This documentation becomes critical evidence when chargebacks occur, helping merchants win disputes by proving the transaction was legitimate and authorized. Additionally, PostAffiliatePro’s integration with major payment processors ensures seamless communication and faster resolution of disputes.

For merchants operating in high-risk industries or with high transaction volumes, PostAffiliatePro’s proactive approach to chargeback prevention is invaluable. The platform helps merchants maintain healthy merchant account status by keeping chargeback rates low, avoiding the penalties and restrictions that come with high dispute rates. By combining advanced fraud prevention, detailed documentation, and comprehensive transaction monitoring, PostAffiliatePro enables merchants to accept payments confidently while protecting their revenue from chargebacks.

Understanding how chargebacks work is essential for protecting your business and maintaining a healthy merchant account. The chargeback process involves multiple stages, from initial dispute through final resolution, and can take 30-120 days to complete. Chargebacks cost merchants far more than just the transaction amount—they include fees, operational costs, and potential damage to merchant account status. By implementing proven prevention strategies such as clear communication, excellent customer service, fraud prevention tools, and prompt order fulfillment, merchants can significantly reduce chargeback rates. When chargebacks do occur, responding quickly with strong evidence is critical for winning disputes. Platforms like PostAffiliatePro provide the tools and documentation needed to prevent chargebacks and win disputes when they occur, making them essential for merchants serious about protecting their revenue and maintaining long-term business success.

PostAffiliatePro's advanced fraud prevention and transaction monitoring tools help you identify and prevent chargebacks before they happen. Reduce dispute rates, protect your revenue, and maintain healthy merchant relationships with our comprehensive affiliate management platform.

The reason for a chargeback is that a product has been returned or a sale has failed. Find out more about chargeback in the article.

Learn the complete chargeback timeline from dispute initiation to final resolution. Understand the 30-90 day process, merchant response deadlines, and how to ma...

Post Affiliate Pro automatically handles refunds and chargebacks by adjusting affiliate commissions accordingly. Protect your business from paying commissions o...

Join our community of happy clients and provide excellent customer support with Post Affiliate Pro.

Cookie Consent

We use cookies to enhance your browsing experience and analyze our traffic. See our privacy policy.