How to Calculate Return on Investment (ROI)

Learn how to calculate ROI with step-by-step formulas, real-world examples, and advanced techniques. Master return on investment calculations for better financi...

10 min read

Discover what constitutes a good ROI based on risk tolerance, investment type, and financial goals. Learn industry benchmarks, historical averages, and how to set realistic investment expectations.

A good return on investment depends on individual expectations and risk tolerance. Generally, 7% annually is considered solid based on historical S&P 500 averages, while 3-5% suits conservative investors, 7-10% for moderate risk, and 10%+ for aggressive investors.

Return on investment is a fundamental metric that measures the profitability of an investment relative to its cost. However, determining what constitutes a “good” ROI is highly subjective and varies significantly based on individual circumstances, investment objectives, and market conditions. The concept of a good return has evolved considerably in 2025, with investors now considering multiple factors beyond simple percentage gains, including inflation-adjusted returns, risk-adjusted performance, and alignment with personal financial goals. Understanding the different benchmarks and expectations across various investment categories is essential for making informed financial decisions and building a sustainable investment strategy.

The most widely recognized benchmark for investment returns comes from the S&P 500 index, which has historically delivered approximately 10% annual returns when adjusted for inflation dating back to the late 1920s. However, when accounting for inflation, the real return typically settles around 7% per year, which has become the standard expectation for long-term equity investors. This 7% benchmark serves as a critical reference point for evaluating investment performance across different asset classes and time horizons. It’s important to note that this figure represents an average over extended periods, meaning individual years can vary dramatically, with some years delivering negative returns while others exceed 15% or more. The consistency of this benchmark over nearly a century of market data provides investors with a reliable baseline for setting realistic expectations, though past performance does not guarantee future results in today’s dynamic market environment.

Set up advanced tracking in minutes. No credit card required.

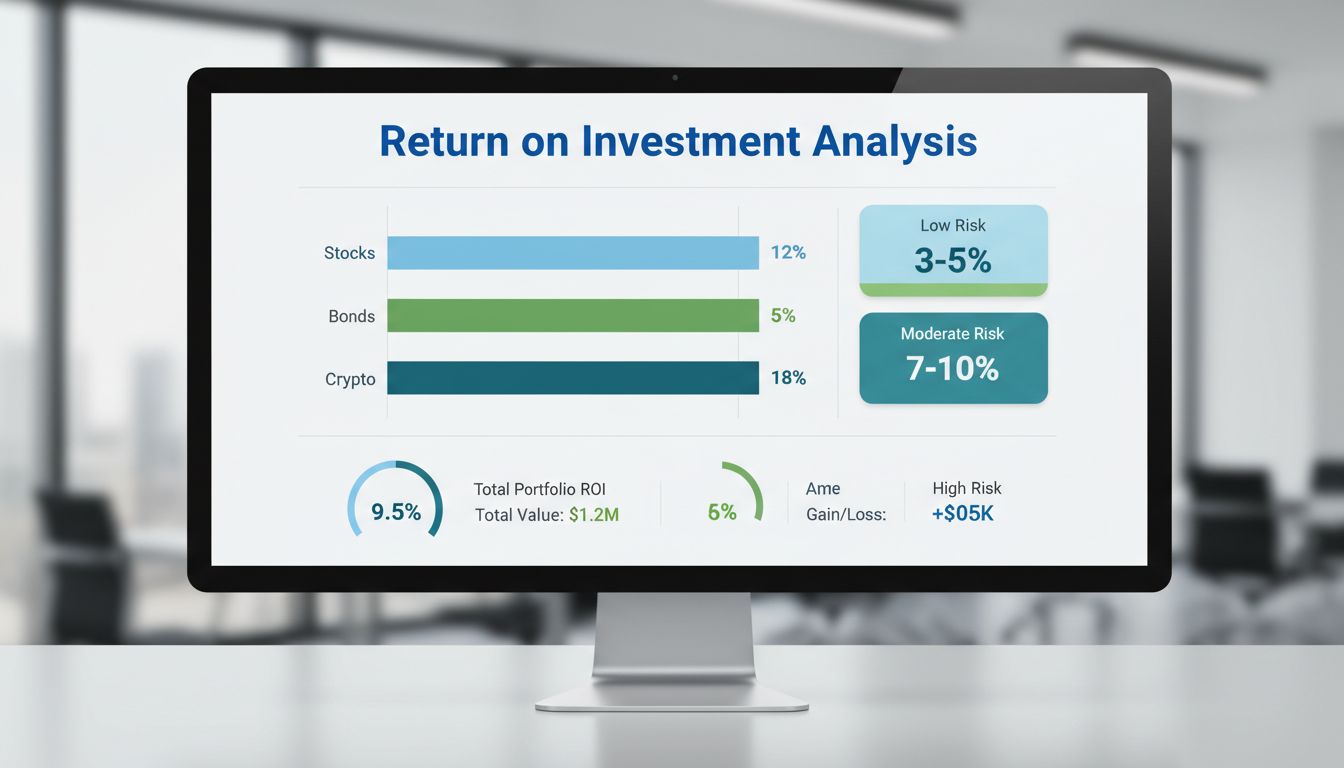

Different investment types carry varying levels of risk and corresponding return expectations. Understanding these categories helps investors align their portfolio allocation with their personal risk tolerance and financial objectives. The following framework provides a comprehensive overview of typical return expectations across the investment spectrum:

| Investment Category | Expected Annual Return | Risk Level | Time Horizon | Best For |

|---|---|---|---|---|

| Bonds & Fixed Income | 3-5% | Very Low | 5-10 years | Conservative investors, retirees |

| Index Funds (S&P 500) | 7-10% | Low-Moderate | 10+ years | Long-term wealth building |

| Dividend Stocks | 6-9% | Moderate | 5-15 years | Income-focused investors |

| Growth Stocks | 10-15% | Moderate-High | 10+ years | Aggressive growth seekers |

| Emerging Markets | 8-12% | High | 10+ years | Risk-tolerant investors |

| Cryptocurrencies | Highly Variable | Very High | Short-term | Speculative investors |

| Real Estate | 8-12% | Moderate | 15+ years | Long-term investors |

| Private Equity | 12-20%+ | Very High | 7+ years | Accredited investors |

For risk-averse investors, particularly those approaching retirement or requiring capital preservation, returns in the 3-5% range are considered excellent and appropriate. This category includes stable bonds, Treasury securities, high-yield savings accounts, and conservative balanced funds that prioritize capital safety over aggressive growth. These investments are designed to provide steady, predictable income streams with minimal volatility, making them ideal for investors who cannot afford significant portfolio fluctuations. The lower return expectations reflect the reduced risk exposure and the trade-off between safety and growth potential. Many financial advisors recommend that retirees and those within five years of retirement maintain a substantial portion of their portfolio in these conservative instruments to ensure they can meet their immediate financial obligations without being forced to sell during market downturns. In 2025, with interest rates stabilizing at higher levels than previous years, conservative investments have become more attractive, offering better yields than they did during the low-rate environment of the 2010s and early 2020s.

Be the first to know about new features and product updates.

The moderate risk category represents the sweet spot for many investors, particularly those with a 10-15 year investment horizon and a balanced approach to growth and stability. This range encompasses diversified stock portfolios, index funds tracking major market indices, and balanced mutual funds that combine stocks and bonds in strategic allocations. Achieving 7-10% annual returns typically requires a disciplined approach to portfolio management, including regular rebalancing, cost minimization through low-fee index funds, and maintaining consistent investment contributions through market cycles. This return range aligns closely with historical market averages and represents what most financial planners consider a realistic expectation for well-constructed, diversified portfolios. The moderate risk approach acknowledges that market volatility will occur but maintains that staying invested through market cycles historically produces superior long-term results compared to attempting to time the market. Investors pursuing this strategy benefit from compound growth over extended periods, where even modest annual returns compound into substantial wealth accumulation when given sufficient time.

Investors with higher risk tolerance and longer time horizons may target returns exceeding 10% annually through exposure to growth stocks, emerging markets, and alternative investments. Achieving these elevated returns requires accepting significantly higher volatility and the possibility of substantial short-term losses, including potential drawdowns of 20-30% or more during market corrections. The 10% rule, popularized by financial experts, recommends limiting speculative investments to no more than 10% of total invested capital, ensuring that even if these high-risk bets fail completely, the overall portfolio remains protected. This strategy is most appropriate for investors who have already established a solid foundation of conservative and moderate investments and can afford to take calculated risks with a portion of their capital. High-return investments include individual growth stocks, technology sector funds, cryptocurrency holdings, and venture capital opportunities, each carrying distinct risk profiles and requiring different levels of expertise to manage effectively. The key to success in this category is maintaining discipline, avoiding emotional decision-making during market volatility, and ensuring that aggressive positions don’t exceed predetermined risk thresholds.

Beyond simple percentage returns, sophisticated investors increasingly focus on risk-adjusted returns, which measure how much return was generated per unit of risk taken. A 20% return achieved with extreme volatility may actually be inferior to a 10% return achieved with minimal volatility when evaluated on a risk-adjusted basis. The Sharpe ratio and other risk-adjusted metrics help investors understand whether they’re being adequately compensated for the risks they’re taking. A 20% annualized return is exceptionally rare as a sustained, risk-adjusted figure for broad portfolios and typically requires either exceptional skill, significant leverage, or concentrated bets that carry substantial downside risk. Most wealthy investors achieve superior returns through a combination of large initial capital, selective high-conviction investments, strategic use of leverage, access to private market opportunities, and the benefit of long-term compounding. Understanding that exceptional returns often come with exceptional risks helps investors maintain realistic expectations and avoid chasing unrealistic performance targets that could lead to poor decision-making and significant losses.

Determining what constitutes a good return for your specific situation requires honest assessment of several key factors. Your investment time horizon significantly influences appropriate return expectations—investors with 30+ years until retirement can afford to pursue higher-risk strategies, while those within 5-10 years of retirement should prioritize capital preservation. Your financial obligations and emergency fund status matter considerably; investors without adequate emergency reserves should maintain more conservative positions to avoid forced selling during market downturns. Your income stability and ability to continue making regular investments affects your risk capacity, as those with stable income can weather market volatility better than those with uncertain earnings. Your overall financial picture, including existing assets, liabilities, and other income sources, determines how much risk you can appropriately take with investment capital. Finally, your emotional tolerance for volatility is crucial—there’s no point pursuing a strategy that will cause you to panic-sell during market corrections, as this typically locks in losses at the worst possible time.

Once you’ve established realistic return expectations aligned with your personal circumstances, the next step is implementing a disciplined investment strategy and monitoring progress systematically. Dollar-cost averaging, where you invest fixed amounts at regular intervals regardless of market conditions, helps reduce the impact of market timing and removes emotion from the investment process. Rebalancing your portfolio periodically—typically annually or when allocations drift significantly from targets—ensures you maintain your intended risk profile and forces you to buy low and sell high in a systematic way. Tracking your actual returns against appropriate benchmarks helps you evaluate whether your strategy is working as intended and whether adjustments are needed. It’s important to compare your returns to relevant benchmarks rather than arbitrary targets; a 7% return on a conservative portfolio might significantly outperform expectations, while the same return on an aggressive portfolio might indicate underperformance. Regular review of your investment strategy, at least annually or when major life changes occur, ensures your approach remains aligned with your evolving goals and circumstances.

Just as investment returns depend on strategy and management, affiliate program success requires the right platform. PostAffiliatePro helps you track, optimize, and maximize your affiliate marketing ROI with industry-leading commission management and real-time analytics.

Learn how to calculate ROI with step-by-step formulas, real-world examples, and advanced techniques. Master return on investment calculations for better financi...

Discover the essential affiliate marketing metrics and KPIs you need to track for success. Learn ROI, CTR, conversion rates, CPA, and more with detailed explana...

Return on investment (ROI) is a measure used to determine the profitability of your investments. It provides valuable insight into money efficiency, especially ...

Join our community of happy clients and provide excellent customer support with Post Affiliate Pro.

Cookie Consent

We use cookies to enhance your browsing experience and analyze our traffic. See our privacy policy.