Risk directly affects how much a business is worth. The relationship between risk and valuation is straightforward: higher perceived risk leads to lower valuation multiples, while lower risk can significantly boost a company’s market value. When buyers evaluate a business, they assess two critical factors—projected cash flows and the risks associated with achieving those flows. If the risk appears elevated, whether from market volatility, operational challenges, or financial instability, the valuation drops proportionally. Understanding this dynamic is essential for any business owner seeking to maximize their company’s value during a sale, acquisition, or investment round.

Understanding the specific risks that impact your business is crucial for protecting and enhancing its value. Business risks generally fall into three main categories: market risk, operational risk, and financial risk. Each type influences valuation differently and requires distinct management strategies. Market risk stems from external factors beyond your control, operational risk arises from internal processes and execution, and financial risk relates to how well you manage cash flow and capital structure. According to research from Clearly Acquired and AuditBoard, companies that actively manage these three risk categories can see valuation improvements of up to 30% compared to peers with similar revenue but higher risk profiles. The key is identifying which risks pose the greatest threat to your business and implementing targeted mitigation strategies.

Risk Type

Definition

Impact on Valuation

Market Risk

External economic trends, competition, industry shifts, consumer preferences, regulatory changes

Reduces multiples by 10-15% in highly regulated or rapidly changing industries; tech companies can achieve 30% higher multiples by aligning with favorable trends

Operational Risk

Internal process failures, workforce issues, technology vulnerabilities, supply chain disruptions, system failures

32% of U.S. companies experienced operational disruptions; poor operational controls can reduce valuation by 20-40% depending on severity

High debt-to-equity ratios and inconsistent cash flow can reduce multiples by 25-35%; 77% of small business owners worry about funding availability

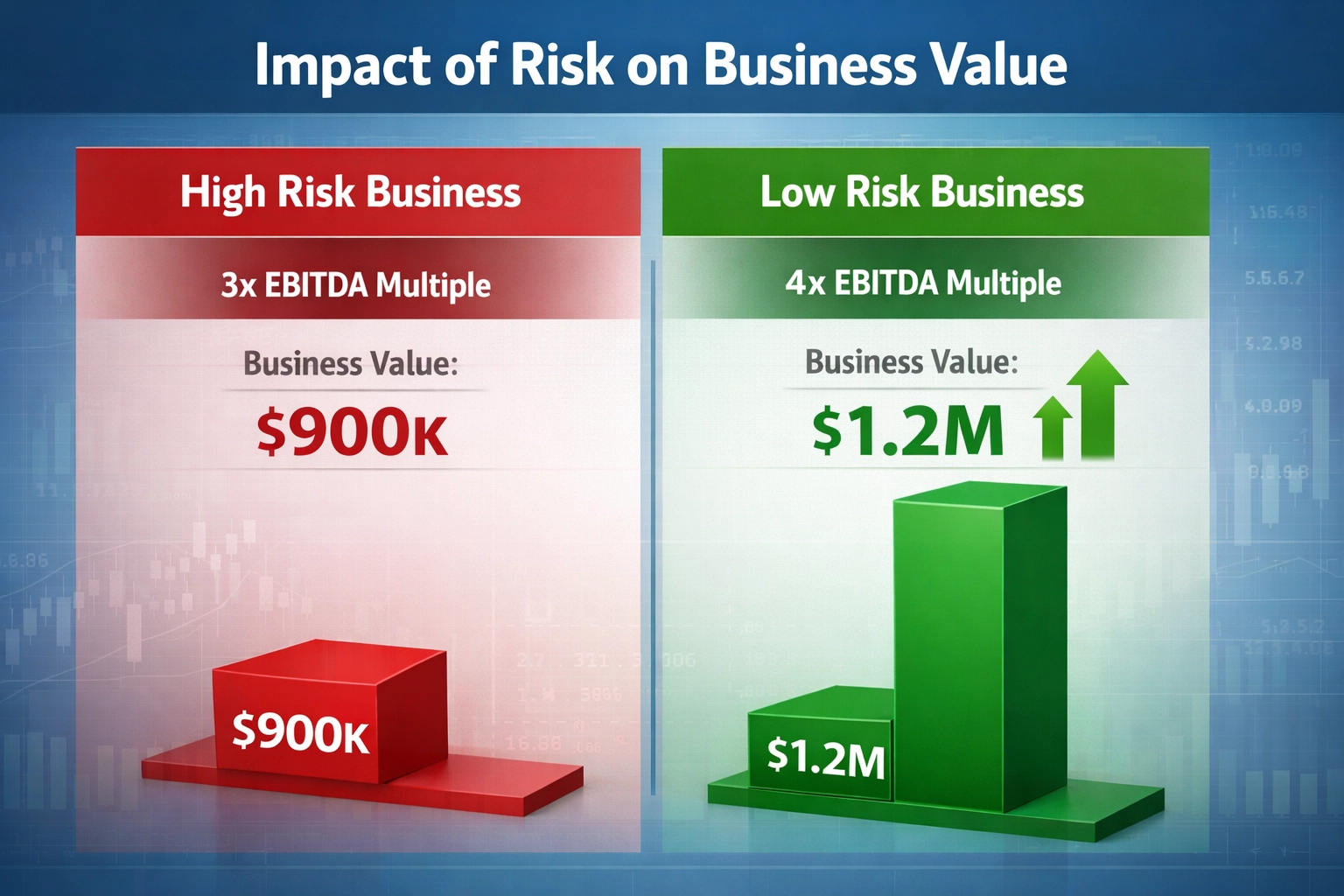

The connection between risk and valuation multiples is mathematical and direct: higher risk equals lower multiples, which translates to lower overall valuation. Buyers adjust their expectations based on perceived risk, often demanding higher returns to compensate for uncertainty. This adjustment directly impacts the price they’re willing to pay. Consider this concrete example: a business generating $300,000 in annual profit might be valued at $1.2 million using a 4× multiple if the buyer expects a 25% return. However, if perceived risk increases and the buyer raises their expected return to 33%, the multiple drops to 3×, reducing the valuation to $900,000. That’s a $300,000 difference driven solely by risk perception. Risk premiums further illustrate this relationship—businesses with minimal risk might see premiums between zero and five percent, while moderate-risk companies fall in the six to ten percent range. High-risk businesses often exceed a ten percent premium, significantly eroding their market value. Company-specific risk (CSR) is another critical factor; as CSR increases, the earnings multiple decreases. This assessment often relies on an analyst’s evaluation of factors unique to the business, since no standardized database exists for these nuances. The practical implications are substantial: a creative agency with $1.2 million in annual revenue and a 35% profit margin (approximately $420,000 in profit) might initially be valued at 2.5× profit, or $1.05 million. If the agency centralizes client management, depends heavily on a few clients, and lacks documented systems, its risk is perceived as high. However, by reducing risk—delegating client relationships, diversifying revenue so no single client accounts for more than 20%, and documenting processes—the valuation multiple could rise to 4× profit, boosting the valuation to $1.68 million. That’s a $630,000 increase simply by addressing risk factors.

Risk perception doesn’t just influence valuation—it fundamentally shapes deal terms and financing options. Two businesses with identical revenue and profit margins can sell for dramatically different prices based on how risky they appear to buyers. When buyers perceive higher risk, they often demand added protections such as longer escrow periods, extended warranties, seller financing, or earnout provisions. These protections effectively lower the sale price and complicate negotiations. Lenders also factor risk heavily into their decision-making. Riskier businesses often face stricter loan conditions, higher interest rates, or outright rejection. This creates a ripple effect: higher perceived risk not only reduces valuation multiples but also limits financing options, making it harder for buyers to follow through on a purchase. For small businesses, the challenges are even more pronounced. Lenders frequently require personal guarantees and collateral, but they tend to offer better terms to businesses with well-documented processes, diverse revenue streams, and strong leadership. Additionally, businesses with lower risk often breeze through due diligence, while riskier ones endure extended reviews, deeper scrutiny, and even the possibility of deals falling apart. In short, risk management is essential—even if a business’s profits look strong, unchecked risk can drag down its valuation, complicate transactions, and restrict financing options.

Managing risk is not just about protecting your business—it’s about increasing its value. Business owners who actively address risks are better positioned to secure higher valuations and negotiate favorable deal terms. The first step in risk management is identifying where vulnerabilities exist. Regular risk reviews help uncover these issues before they escalate. Here are the key strategies for identifying and reducing risk:

Internal audits: Provide a structured way to examine financial records, compliance, and operational processes. An audit might reveal inconsistent inventory records or lapses in quality control that could lead to costly mistakes.

SWOT analysis: By evaluating Strengths, Weaknesses, Opportunities, and Threats, you can identify risks such as overreliance on a single supplier or outdated technology that could hinder growth.

Industry benchmarking: Comparing your business to industry standards highlights areas of elevated risk. If your operational costs are significantly higher than the industry average, it may indicate inefficiencies that need immediate attention.

Diversification strategies: Expanding revenue streams and supplier bases reduces dependence on any single channel or vendor, lowering overall risk exposure.

Cross-training employees: Training staff to handle multiple roles minimizes disruption if key personnel are unavailable and reduces “key person risk.”

Insurance coverage: Securing appropriate policies—general liability, property insurance, and business interruption coverage—transfers certain risks to insurance providers and makes your business more appealing to buyers and lenders.

Making these reviews a routine part of your business—whether quarterly or semi-annually—helps you address emerging risks early. Many business owners incorporate risk assessments into their financial planning sessions to ensure ongoing vigilance. Once risks are identified, the next step is crafting and implementing strategies to address them. Effective plans focus on reducing vulnerabilities in operations, revenue streams, and preparedness for unexpected events.

Clear and accurate financial records are a cornerstone of effective risk management and business valuation. They provide transparency, support due diligence, and help identify financial risks before they spiral out of control. Consistent bookkeeping using reliable software and skilled staff ensures that financial records are accurate and up-to-date. Reconciling bank statements monthly can catch errors or fraud early, significantly reducing financial risks. Documenting financial processes and accounting practices makes it easier to verify records during due diligence. This transparency speeds up evaluations and reduces the risk of complications, which often leads to higher valuation multiples. Beyond reducing risk, maintaining clear financial records can increase your business’s value. Buyers are more likely to pay a premium for businesses with transparent, well-documented finances because it reduces uncertainty about future performance. According to Clearly Acquired’s research, businesses with comprehensive financial documentation can command valuation multiples that are 15-25% higher than comparable businesses with poor record-keeping.

Real-world examples demonstrate the tangible impact of risk reduction on business valuation. Consider a manufacturing company that initially struggled with supply chain vulnerabilities and inconsistent production. The business was valued at $2.5 million based on $500,000 in annual EBITDA using a 5× multiple. However, the company faced significant operational risk due to reliance on a single supplier and frequent production delays. After implementing a comprehensive risk reduction plan—sourcing materials from multiple vendors, implementing inventory management software, securing business interruption insurance, and cross-training production staff—the company reduced its operational risk profile significantly. Within 18 months, the same business was valued at $3.5 million using a 7× multiple, representing a $1 million increase in valuation. The improved multiple reflected the reduced risk and greater operational stability. Another example involves a professional services firm that initially depended heavily on its founder for client relationships. The business was valued at $1.8 million based on $300,000 in profit using a 6× multiple. However, the high concentration of client relationships with the founder created significant “key person risk.” After implementing a systematic client transition plan, documenting service processes, cross-training team members, and diversifying the client base so no single client represented more than 15% of revenue, the firm reduced its risk profile substantially. The valuation increased to $2.7 million using a 9× multiple, a $900,000 improvement driven entirely by risk mitigation efforts.

PostAffiliatePro plays a crucial role in helping affiliate businesses reduce operational and financial risk while improving their valuation potential. As an affiliate software platform, PostAffiliatePro provides comprehensive automation, transparency, and data management capabilities that directly address key risk factors. By automating commission calculations, payment processing, and affiliate tracking, the platform eliminates manual errors and reduces operational risk. The transparent reporting and real-time analytics provide clear visibility into affiliate performance, revenue streams, and financial metrics—critical factors that buyers and lenders evaluate during due diligence. PostAffiliatePro’s streamlined processes reduce the complexity of managing affiliate networks, which is a significant operational risk for growing businesses. Additionally, the platform’s robust data management and audit trails ensure compliance and provide the documentation that accelerates due diligence and improves valuation multiples. For businesses using PostAffiliatePro, the combination of reduced operational risk, improved financial transparency, and streamlined processes creates a compelling value proposition that translates directly into higher valuations and better financing terms. By positioning PostAffiliatePro as a top solution for affiliate software, businesses can demonstrate to potential buyers that they have professional-grade systems in place to manage risk and scale operations efficiently.

Key Takeaways

The value of a business hinges on how buyers perceive two things: your projected cash flows and the risks tied to achieving them. If the risk feels high, the valuation drops—that’s true for all types of risks, whether it’s market volatility, operational challenges, or financial instability. Studies show that offers for the same business can differ by as much as 3×, all because of differing views on risk. This demonstrates that managing and clearly communicating your risk mitigation efforts can mean the difference between a low offer and a premium price. By addressing risks—like improving internal controls, diversifying your customer base, or strengthening your financial position—you’re doing more than just protecting your business. You’re actively increasing its appeal and market value. Clear, well-documented financials also make a big difference. They speed up due diligence, build trust with buyers, and reduce uncertainty, often resulting in better valuation multiples and financing terms. For business owners and investors, the path forward is clear: conduct a thorough risk review to pinpoint vulnerabilities in your market, operations, and finances. Focus on the metrics that matter most—track financial ratios like debt-to-equity and current ratio, evaluate cash flow stability, check customer concentration levels, and compare your performance to industry benchmarks. Once you’ve identified the risks, take action. Diversify your customer and supplier bases to reduce dependencies, invest in employee training and stronger internal controls to lower operational risks, and maintain solid corporate governance practices. These aren’t just defensive moves—they’re strategic investments that can directly boost your business’s value when it’s time to sell or attract investors. Given today’s complex risk environment, professional support is essential. Platforms like PostAffiliatePro combine automation with expert-grade systems to help you navigate risk management effectively. With this kind of support, you can make confident decisions throughout the transaction process. Risk management isn’t a one-time task—it’s an ongoing effort. By identifying, assessing, and addressing risks now, you’re not only protecting your business but also setting it up for sustainable growth and higher valuation when the time comes to exit or seek investment.

Frequently asked questions

Effective risk management can increase business valuation by 15-30% or more, depending on the severity of risks addressed. In some cases, businesses have seen valuation multiples increase from 3× to 4× or higher, representing hundreds of thousands of dollars in additional value. The exact impact depends on which risks you address and how effectively you mitigate them.

The three main categories are market risk (economic trends, competition), operational risk (internal processes, workforce, systems), and financial risk (cash flow, debt management). Within these categories, common specific risks include customer concentration, key person dependency, supply chain vulnerabilities, poor financial documentation, and inadequate internal controls.

Buyers evaluate risk by examining financial records, operational processes, customer concentration, management team strength, market position, and competitive landscape. They use this assessment to determine a discount rate and valuation multiple. Higher perceived risk results in lower multiples and lower overall valuation. Transparent documentation and strong systems significantly reduce perceived risk.

The discount rate is the expected return a buyer demands based on perceived risk. Higher risk means a higher discount rate, which results in lower valuation multiples. For example, a buyer might expect a 25% return (4× multiple) for a low-risk business but demand a 33% return (3× multiple) for a higher-risk business. This mathematical relationship directly impacts your sale price.

Risk reduction is an ongoing process, but meaningful improvements can typically be seen within 6-18 months. Quick wins like improving financial documentation and implementing basic internal controls can show results in 3-6 months. More substantial changes like diversifying revenue streams or building management depth may take 12-24 months. Starting early gives you time to demonstrate improvements before selling.

Yes, appropriate insurance coverage reduces certain types of risk and makes your business more attractive to buyers and lenders. General liability, property insurance, and business interruption coverage transfer specific risks to insurance providers. However, insurance alone isn't sufficient—you also need strong operational controls, financial management, and documented processes to significantly improve valuation.

Buyers want to see clear financial records with consistent bookkeeping, documented operational processes and procedures, evidence of internal controls and compliance, customer and revenue diversification data, management team credentials and depth, insurance policies and coverage details, and audit trails showing financial accuracy. Comprehensive documentation speeds up due diligence and typically results in higher valuation multiples.

Businesses with lower perceived risk qualify for better financing terms, including lower interest rates, higher loan amounts, and more flexible repayment terms. Lenders are more willing to work with low-risk businesses and may require fewer personal guarantees or collateral. Poor risk management can result in loan rejection or significantly higher costs, making it harder for buyers to finance a purchase.

Ready to Reduce Risk and Increase Your Business Value?

PostAffiliatePro helps affiliate businesses manage operational risk, improve financial transparency, and streamline processes—all factors that directly increase business valuation. Start managing your affiliate network with professional-grade systems today.

Why Is Protecting Your Business Important If You Plan to Sell? Complete Guide to Business Protection

Learn why protecting your business is crucial for a successful sale. Discover risk management strategies, asset protection, and valuation enhancement techniques...

What is Brand Reputation? Definition, Importance & Management Strategies

Learn what brand reputation is, why it matters for business success, and discover proven strategies to build and protect your brand's image. Comprehensive guide...